Gifting your wealth is perhaps one of the most effective ways to reduce the value of your estate and mitigate a potential Inheritance Tax (IHT) bill for your loved ones.

This is more important than ever, given that Money Marketing states that IHT receipts rose to a record £8.5 billion for 2025/26. This marked the fifth consecutive annual high.

Moreover, from April 2027, pensions and unused death benefits will be included in the scope of IHT, meaning much more of your estate could be subject to tax in the future.

As such, you might have given more thought to the ways you can pass your wealth on to loved ones during your lifetime.

Yet, gifting isn’t always as simple as transferring wealth from one person to another. As a couple, it can be essential to consider which of you should make the gift.

The “right” answer will wholly depend on factors such as:

- The size of each estate

- Your health

- Your regular income.

Read on to learn about some considerations when deciding who should make a gift for IHT purposes.

1. The size of each person’s estate

The first, and perhaps most important, factor to consider is the size of each person’s estate.

As of 2026/27, the standard nil-rate band is £325,000. This means that you can typically pass on the first £325,000 of your estate without incurring IHT.

You can also make use of up to £175,000 via the residence nil-rate band if you leave your main home to a direct lineal descendant.

Additionally, you can benefit from the spousal exemption, which allows you to pass your entire estate to a spouse or civil partner without IHT. They can also inherit your unused nil-rate bands. This potentially gives you a combined IHT-free threshold of £1 million, and the IHT on any wealth you pass to a spouse or civil partner will be calculated after the second person passes away.

Anything above the nil-rate bands is typically taxed at 40%.

However, despite the spousal exemption, it might be more beneficial for the person with the larger estate to make gifts first for several reasons.

First, you might not leave your entire estate to your spouse or civil partner, and some assets may pass directly to other beneficiaries, making them potentially subject to IHT.

Additionally, if you make gifts that exceed your annual gifting exemption of £3,000, you must survive for seven years after making the gift before they become exempt from IHT (more on this later).

If you pass away within that time, IHT on that amount is calculated on the first death, not the second.

As such, it is still beneficial for couples to reduce the value of the larger estate and bring it closer to the nil-rate bands, where possible. This is even more important if you are not married or in a civil partnership and won’t benefit from the spousal exemption.

2. The relative health of both parties

It’s also worth thinking carefully about health and life expectancy. This is because many lifetime gifts are treated as “potentially exempt transfers” (PETs).

These allow you to give a potentially unlimited amount of your wealth to loved ones, provided you survive for more than seven years from the date of the gift.

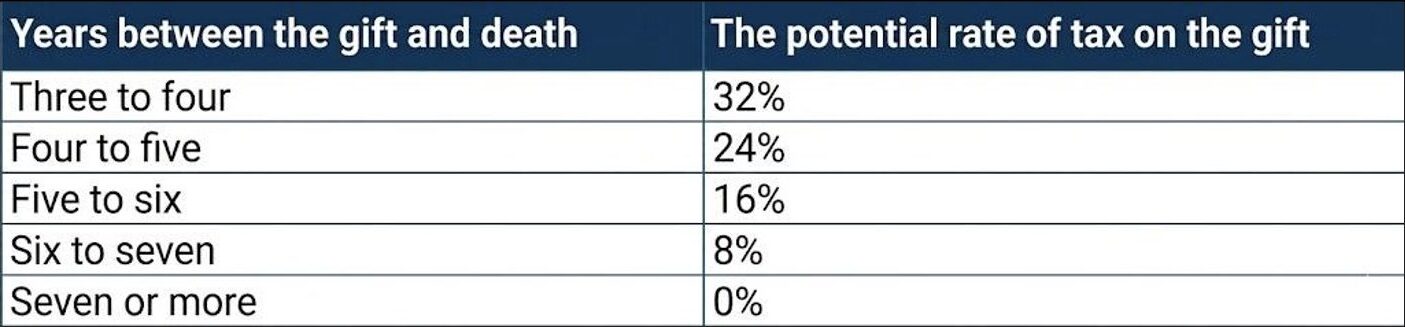

If you pass away within this period, the IHT rate your beneficiaries pay could be reduced on a sliding scale known as “taper relief”.

The table below demonstrates how much tax loved ones might pay depending on how long you survive after making a significant gift.

This means that if one person in a couple is in much better health or more likely to survive the full seven-year period, it might be wiser for them to make the gift.

For example, if your partner has serious health concerns while you’re in good health, making a large PET from your estate could give it a better chance of falling outside the scope of IHT.

Granted, this can be a sensitive topic of conversation, and it’s challenging to predict what might happen in the future.

Still, it may be sensible to consider whether the person making the gift is likely to survive long enough for tax mitigation.

3. The regular income of each person

One-off gifts can be an effective way to reduce the overall value of your estate, though you might have overlooked the “gifting from income” rules.

These potentially limitless gifts can be free from IHT, provided they meet certain strict criteria.

You must be able to demonstrate that the gifts are made from your additional income rather than from capital or savings. What’s more, they can’t affect your standard of living.

This means that if you have enough to cover your daily expenses comfortably and still have some leftover income each month, you could give it to a child or grandchild.

Just remember that the gifts must be regular, ideally monthly or yearly, so you may need to keep records to prove this.

Due to this, it might be worth considering which person in the couple has the most surplus income.

If you receive a larger pension or rental income and consistently have money left after meeting normal living costs, you might be better placed to make use of this exemption.

Meanwhile, if your spouse draws from capital to make the payments, the exemption likely won’t apply, and the gift would be treated as a PET and remain within their estate for seven years.

Get in touch

We could help you review your estate, assess the potential IHT implications, and decide how gifting might fit into your wider financial plan.

Please get in touch to find out how our team of VouchedFor Top Rated planners could help today.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.