In October 2025, the Child Poverty Action Group released its Cost of a Child in 2025 report. The organisation found that raising a child to age 18 costs £250,000 for a couple and £290,000 for a lone parent.

Pre-school childcare can be especially expensive. According to Good Nurseries, the cost of full-time childcare from birth to age four could exceed £50,000.

Two types of government help are available to cover childcare costs for working parents, but caveats exist, and higher-earning couples could find they fall into the so-called “£100,000 tax trap”.

Keep reading for more about the help available, when the “trap” applies, and how to mitigate its impact.

You might be eligible for two main types of childcare support

1. Funded childcare hours

Working parents in England can claim 30 hours of funded childcare.

Note: Different schemes apply in Scotland, Wales, and Northern Ireland.

To be eligible for the free hours in England, you and your partner (if you have one) will need to be employed, working at least 16 hours, or earning at least the equivalent of 16 hours at the National Minimum Wage. You must also have an adjusted net income of less than £100,000.

The hours are available for 38 weeks of the year, for children aged nine months to four years. You can apply for the free hours via the government website once your child is 23 weeks old. You’ll receive an 11-digit code to share with your chosen childcare provider.

2. Tax-free childcare

The earnings rules for funded hours also apply to tax-free childcare.

Both you and your partner (if you have one) must be in work earning between the equivalent of 16 hours at the National Minimum Wage and £100,000 (net adjusted).

If you’re eligible for tax-free childcare, you’ll receive a government top-up of £2 for every £8 you save for each child aged 11 or under, up to a maximum of £500 a quarter (£2,000 a year).

The annual figure rises to £4,000 for disabled children aged up to 16.

If you or your partner’s income exceeds £100,000, you could lose more than just your valuable childcare support

Eligibility for both of the above schemes is based on individual (rather than household) income. This means that if you and your partner both earn £99,000 a year – and all other criteria are met – you’ll be eligible for free hours and the tax-free top-up.

If you receive a pay rise, though, and one partner’s income hits £100,001, the childcare help ceases. This is the case even if the other partner earns minimum wage or isn’t working at all.

Sadly, the situation gets worse. This is because the Personal Allowance – the amount you can earn before Income Tax becomes payable – begins to taper once your earnings exceed £100,000.

Income Tax is paid as follows on earnings of:

- Up to £12,570 – No Income Tax payable

- Between £12,571 and £50,270 – 20%

- Between £50,271 and £125,140 – 40%

- £125,141 and above – 45%.

However, for every £2 you earn above £100,000, you lose £1 of your Personal Allowance, and by £125,140, your Personal Allowance is lost entirely. This creates an effective marginal rate of Income Tax of 60% on income between £100,000 and £125,140.

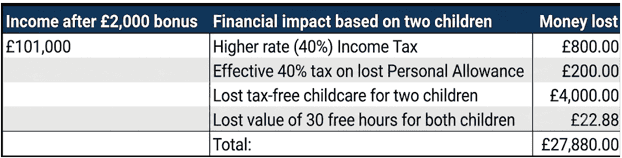

Here’s an example using figures from AJ Bell that illustrates the cost of a £2,000 bonus, taking your earnings from £99,000 to £101,000.

The figures above are based on two working parents with two children, one aged two, the other under two. They show that the impact of a £2,000 bonus taking one parent over the £100,000 threshold could cost almost £28,000 in tax and lost childcare help.

3 ways you could reduce your taxable income and avoid the tax trap

If you or your partner is nearing the £100,000 threshold, there are steps you can take.

1. Increase your pension contributions

Pension contributions are deducted from taxable pay when calculating your adjusted net income.

If your salary is close to £100,000, a relatively small pension top-up could see your income drop below the threshold, allowing you to retain childcare help and avoid the 60% tax trap. You might consider using salary sacrifice if your workplace scheme offers it.

Just remember that if you earn significantly more than £100,000, large increases to your pension contributions could see you exceed the Annual Allowance or limit your financial freedom in the short term, so seeking advice is key.

2. Defer a bonus or a pay rise

While you’ll be delighted to receive a bonus or pay rise, you’ll also want to think about the timing. You might even ask your employer to defer a planned rise.

You’ll need to consider the age of your children and calculate the benefit of the rise against a potential loss of childcare support or a higher tax bill.

3. Make Gift Aid donations

Donations made using Gift Aid also reduce your adjusted net income and could take you below the £100,000 threshold.

This option has the added benefit of allowing you to support a cause you care about with money that might otherwise have been lost to tax.

Get in touch

Childcare is expensive, and the government help available could prove invaluable. As a high earner, you could lose this help and find yourself worse off thanks to the 60% tax trap, so contact us if you need advice.

Please get in touch to find out how our team of VouchedFor Top Rated planners could help today.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance. The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pensions Regulator.